World

UK’s Top 3 Stocks Estimated To Be Undervalued In September 2024

The United Kingdom’s stock market has recently faced challenges, with the FTSE 100 and FTSE 250 indices closing lower due to weak trade data from China and decreased commodity prices impacting major companies. Despite these headwinds, identifying undervalued stocks can present opportunities for investors seeking value in a fluctuating market.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Triple Point Social Housing REIT (LSE:SOHO) | £0.665 | £1.30 | 49% |

| Victorian Plumbing Group (AIM:VIC) | £1.015 | £1.85 | 45.3% |

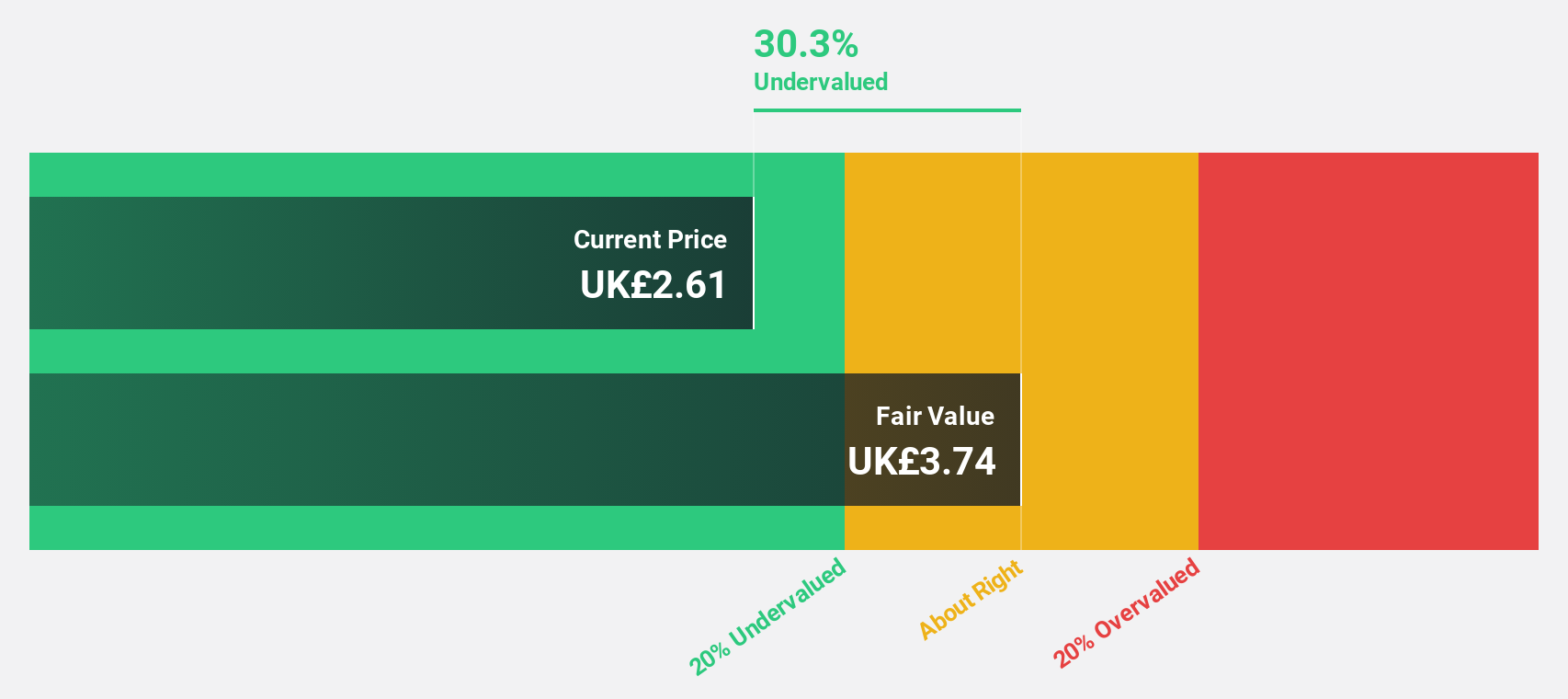

| Topps Tiles (LSE:TPT) | £0.46 | £0.89 | 48.4% |

| Fevertree Drinks (AIM:FEVR) | £7.665 | £14.20 | 46% |

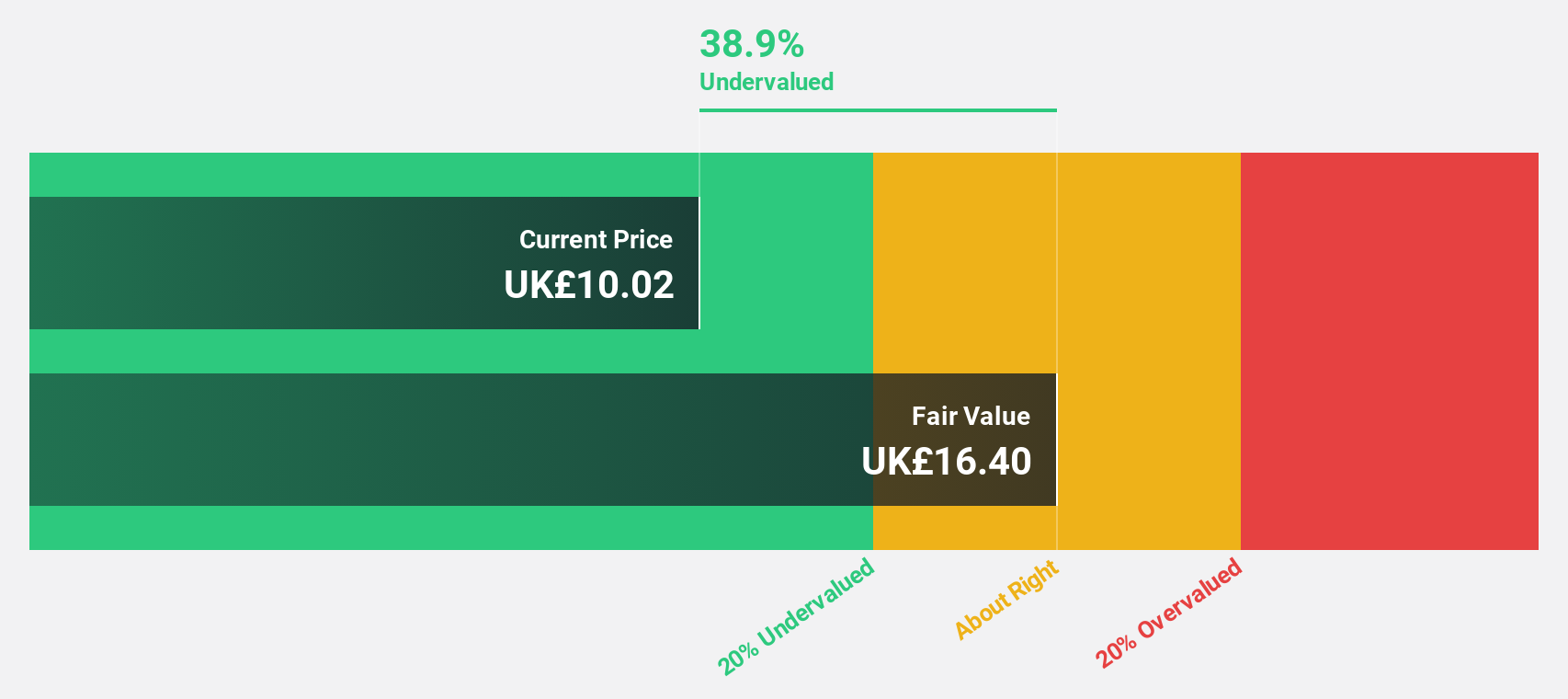

| Informa (LSE:INF) | £8.492 | £16.81 | 49.5% |

| Redcentric (AIM:RCN) | £1.275 | £2.45 | 47.9% |

| Velocity Composites (AIM:VEL) | £0.435 | £0.82 | 47% |

| Tortilla Mexican Grill (AIM:MEX) | £0.52 | £1.01 | 48.4% |

| SysGroup (AIM:SYS) | £0.345 | £0.66 | 47.8% |

| Foxtons Group (LSE:FOXT) | £0.634 | £1.19 | 46.9% |

Let’s take a closer look at a couple of our picks from the screened companies.

Overview: GB Group plc, with a market cap of £796.68 million, offers identity data intelligence products and services across the United Kingdom, the United States, Australia, and internationally.

Operations: The company’s revenue segments include £40.20 million from Fraud, £156.06 million from Identity, and £81.07 million from Location services.

Estimated Discount To Fair Value: 36.4%

GB Group (£3.16) is currently trading significantly below its estimated fair value of £4.96, representing a 36.4% discount. Earnings are forecast to grow at an impressive 92.88% per year, with revenue expected to increase by 6.8% annually, outpacing the UK market’s growth rate of 3.7%. Analysts anticipate a price rise of 33.7%, and the company declared a final dividend of 4.20 pence on July 23, 2024, highlighting its strong cash flow position despite low future return on equity forecasts (3 years: 3.4%).

Overview: Marshalls plc, with a market cap of £830.09 million, manufactures and sells landscape, building, and roofing products in the United Kingdom and internationally through its subsidiaries.

Operations: Revenue segments for Marshalls plc include £284.40 million from Landscape Products, £174.70 million from Roofing Products, and £164.70 million from Building Products.

Estimated Discount To Fair Value: 23.9%

Marshalls plc (£3.29) is trading 23.9% below its estimated fair value of £4.32, indicating undervaluation based on cash flows. Despite a decline in sales to £306.7 million for H1 2024, net income rose to £16.1 million from £13.1 million last year, showing improved profitability. Earnings are forecast to grow significantly at 27.94% per year over the next three years, outpacing the UK market’s growth rate of 14.2%.

Overview: Savills plc, with a market cap of £1.58 billion, provides real estate services across the United Kingdom, Continental Europe, the Asia Pacific, Africa, North America and the Middle East.

Operations: The company’s revenue segments include Consultancy (£464.80 million), Transaction Advisory (£803.60 million), Investment Management (£100.50 million), and Property and Facilities Management (£920.90 million).

Estimated Discount To Fair Value: 22.9%

Savills plc (£11.70) is trading 22.9% below its estimated fair value of £15.17, suggesting it is undervalued based on cash flows. For H1 2024, Savills reported sales of £1.06 billion and net income of £8.3 million, up from £4.8 million last year, reflecting improved profitability despite lower profit margins (1.9% vs 3.8%). Earnings are forecast to grow significantly at 33.29% per year over the next three years, outpacing the UK market’s growth rate of 14.2%.

Seize The Opportunity

- Investigate our full lineup of 52 Undervalued UK Stocks Based On Cash Flows right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St’s portfolio, where intuitive tools await to help optimize your investment outcomes.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Want To Explore Some Alternatives?

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice.

It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Daily horoscope: November 13, 2024 astrological predictions for your star sign

Why this ‘cinematic’ Pembrokeshire beach is among Britain’s best for a winter walk

See the ‘buzzing’ South Wales Christmas market named among best in the UK

Top Blair adviser who said ‘we don’t need small farmers’ disowned by Starmer

New report reveals UK’s best and worst places to take your driving test | GoCompare News

Ukraine-Russia war latest: North Korea ratifies military pact with Moscow

Starmer pledges huge cut to UK emissions as assisted dying Bill looms – live

UK can strike Trump trade deal and rebuild EU relations, says top economist

Unemployment rises as pay growth slows again